The Role of Banks in Tackling Climate Change

Climate change refers to long-term shifts in temperatures and weather patterns. While such shifts can be natural, the overwhelming scientific consensus is that the climate changes observed since the mid-20th century are primarily driven by human activities. Climate risk encompasses the potential for negative consequences on societies and ecosystems due to the impacts of climate change. It involves analysing the likelihood and severity of these impacts and the ability to respond to them. These risks are becoming increasingly apparent worldwide, manifesting in a growing number of climate-driven disasters. Banks have a multifaceted and crucial role to play in tackling climate change. As primary providers of capital and key players in the financial system, they can significantly influence the transition towards a low-carbon and climate-resilient economy

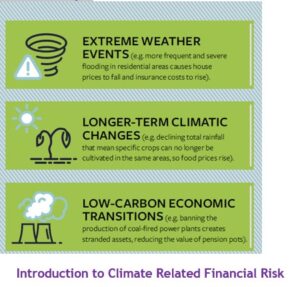

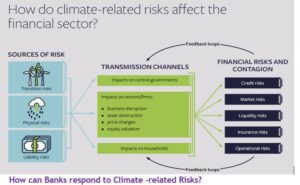

1. Physical Risks: Physical risks concern the physical damage to firms and assets from climate-related shocks and stresses, such as rising temperatures, heavier rainfall or rising sea levels. The costs of these damages may be transmitted to a financial institution when they have an interest in a project – for example, if a bank provided a mortgage to a home on a floodplain or a pension fund financed infrastructure that was damaged by a storm. The costs may also be transmitted indirectly through damages to firms and households in which the financial institution has an interest – for example, if a sovereign wealth fund purchased municipal bonds from a city that has been struck by drought or cyclones

2. Transition Risks: Transition risks concern the potential loss of value of firms and assets because of the low-carbon economic transition. More stringent climate policies, the emergence of new technologies and changing consumer demand could potentially impact the lifespan or profitability of high-carbon projects. The costs and losses will flow through to financial institutions. Several cities and countries have announced plans to ban the sales of internal combustion engines. This will affect financial institutions that have outstanding credit with or hold shares in oil majors and ICE manufacturers. However, financial institutions that have invested in or lent money to electricity utilities and electric car manufacturers will benefit from the transition. o rising sea levels.

3. Liability Risks: Liability risks are financial costs and losses to financial institutions that may occur if parties seek compensation for the damages suffered from climate impact. Insurance companies are already facing higher liabilities from weather-related losses. Large emitters are also facing legal action for the climate impacts of their historical greenhouse gas emissions.

How can Banks respond to Climate -related Risks?

The Basel Committee on Banking Supervision (BCBS) is the primary global standard setter for the prudential regulation of banks. It has introduced Basel III, a global voluntary framework for regulating the financial sector. Basel III has three pillars: minimum capital requirements, supervisor review and market discipline. Improved disclosure of climate-related financial risks would strengthen the ability of central banks to act under all three of these pillars.

- Minimum Capital Requirement: – Financial institutions can understand current and expected liabilities more reliably, and have enough reserves to meet them in a timely manner.

- Supervisory Review: – Central banks and supervisors can incorporate climate-related risks when running stress-testing scenarios to assess overall financial stability.

- Market Discipline: – Financial institutions can identify climate risks on their balance sheets and loan portfolios more effectively, and allocate capital accordingly.

There is growing recognition that central banks’ ability to set expectations and binding rules will be relevant for managing systemic financial risks that may arise from climate change. There are also debates on the potential role of financial regulators to actively promote green finance and reduce unsustainable economic activities.

What are enhanced capital and liquidity requirements?

Financial institutions are required to have capital and liquidity buffers, so that their reserves are in proportion to the risks they take. These reserves ensure that banks have the ability to meet the short-term demand for cash from their customers (liquidity) and any short-term losses to their own business (capital).

How can Central Banks incorporate Climate Change?

Central banks can add a ‘green-supporting factor’ or ‘dirty-penalising factor’ to capital and liquidity requirements. In other words, financial institutions might be required to hold more reserves if they are exposed to climate-related physical, transition and liability risks. This creates an incentive for financial institutions to shift to lower-carbon, climate-resilient loans and investments, as they have more opportunities to generate revenues.

However, there is much debate around adjusting capital and liquidity requirements in favour of ‘green’ and against ‘dirty’ assets. For instance, while transition risks may affect ‘dirty’ assets more severely, some ‘dirty’ companies are highly capitalised, have strong management and a credible long-term strategy might manage the transition well. Meanwhile, some ‘green’ companies may also be vulnerable to transition risks if their business models are based on new technologies that have yet to be proven at scale.

1. Basel III- Pillar 1

Capital Requirements: – Sufficient reserves for banks to meet any short-term losses to their own business. Minimum requirements are usually set by the financial regulator based on a risk assessment of the banks’ assets.

Liquidity Requirements: – Sufficient reserves for banks to meet any short-term demand for cash from their customers. Minimum requirements are usually set by the financial regulator according to typical cash outflows or obligations over a defined period.

2. Basel III – Pillar 2

Central banks use “stress testing” as their main supervisory tool. Stress tests can reveal systemic vulnerabilities that need risk mitigation measures. Central banks can use climate-related financial disclosures to more robustly model how climate shocks might affect the financial sector.

What Might Stress Testing Reveal?

- Flooding in urban areas might affect banks with high exposure to mortgages.

- Commitments to phase out coal might leave investors with stranded assets.

- The rise of new technologies might affect the profitability of established companies.

3. Basel III –Pillar 3

Financial institutions can use climate-related risk disclosures to make more informed decisions about how they will allocate their own funds. Armed with this information, they can reduce their own exposure to climate-related risks by withdrawing finance or by encouraging clients to mitigate these risks. The disclosures therefore also create incentives for households and firms to act on climate change so that they can secure finance more easily. Market discipline among financial institutions can therefore reinforce regulation and supervision by central banks.

Conclusion

How can central banks support a low-carbon transition?

Central banks and other regulators have an important role to play in managing climate-related financial risks, but also facilitating a low-carbon transition. For example:

(a) Green Credit Allocation:-Central banks or other regulators can introduce sustainable finance taxonomies that classify which activities qualify as ‘green’ or ‘grey’. Financial institutions can use these taxonomies to make more informed lending and investment decisions, improving comparability and accountability across the sector. A sustainable finance taxonomy can also be linked to capital and liquidity requirement.

(b) Green Quantitative Easing: – Central banks often purchase assets to stimulate the economy. Many favour bonds over equity or project loans. Their purchases are therefore biased towards incumbents in carbon-intensive industries, such as manufacturing and electricity generation, which are more likely to issue bonds. Central banks could green their balance sheets by purchasing other types of assets, such as equities, or preferentially purchasing green bonds.

Authored by:

Ujjwal Kant

Chief Manager (Faculty)

Zonal Learning Centre

Lucknow

Union Bank of India