INDIA’S ASSET MANAGEMENT LANDSCAPE: THE PATH TO FINANCIAL EMPOWERMENT

Introduction:

Projected to become the world’s third-largest economy within the next decade, India has demonstrated robust economic expansion, significantly outpacing global averages with GDP growth over six percent annually since 2012. This economic vitality has fueled rising incomes and fostered a strong savings culture, with gross national savings representing a substantial portion of the national disposable income, far exceeding rates seen in many developed nations.

Despite this high propensity to save, traditional financial avenues have historically captured the lion’s share of household financial assets. The asset management sector, particularly the mutual fund segment, while growing rapidly, started from a relatively small base. Initial estimates placed the industry AUM around USD 350 billion in March 2018, part of a broader asset management sphere (including pensions and alternatives) valued at roughly USD 550-650 billion then.

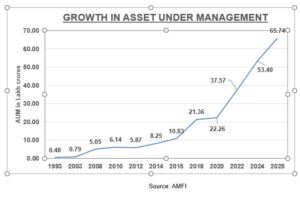

However, the landscape has transformed dramatically. By March 2025, the Assets Under Management (AUM) of the Indian mutual fund industry had surged to approximately Rs. 65.74 lakh crore (around USD 780 billion). Over the past ten years, this represents a growth greater than six times. Today, mutual funds represent a significant and growing portion of India’s GDP – reaching a record 18.2% in fiscal 2024 – indicating increasing investor acceptance. This upward trajectory highlights the vast potential for Asset Management Companies (AMCs), supported by rising prosperity, enabling regulations, positive economic forecasts, and favorable demographics, including a large, young population and an expanding middle class. Furthermore, the reach of mutual funds has broadened, with the total number of investor accounts, known as folios, exceeding 23.4 crore by March 2025.

The Industry’s Evolutionary Path: From Monopoly to Mainstream

The journey of India’s mutual fund industry, the heart of the asset management sector, stretches back over sixty years. Its development can be traced through distinct phases, moving from a monopolistic structure to a vibrant, multi-player ecosystem.

Phase 1: The Foundation Period (1964 – 2014)

The inception dates back to 1963 with the government-backed Unit Trust of India (UTI), which launched the first mutual fund product (US-64) in 1964. For over two decades (1964-1987), UTI remained the sole player in a market characterized by limited product choice, conservative investor attitudes, and a focus primarily on urban savers. In an economy dominated by agriculture and bank deposits, mutual funds offered a novel way to channel household savings into capital markets, especially crucial in an environment where inflation often outpaced deposit returns.

From 1987 to 1995, the sector saw the entry of public sector financial institutions, introducing an element of competition. The sweeping economic reforms of the early 1990s provided further impetus. Key regulatory developments during this time included granting statutory powers to the Securities and Exchange Board of India (SEBI) in 1992 and establishing the Association of Mutual Funds in India (AMFI) in 1995. These bodies were instrumental in setting standards for transparency and ethical conduct. By 1995, the industry’s AUM had grown substantially to Rs. 47,000 crore.

A major turning point occurred around the year 2000 with the entry of private sector AMCs (Phase 1C: 1995-2014). This influx sparked innovation, leading to specialized offerings like sector-specific funds, tax-saving Equity Linked Savings Schemes (ELSS), and Fixed Maturity Plans (FMPs). The introduction and popularization of Systematic Investment Plans (SIPs), Exchange Traded Funds (ETFs), and Fund of Funds (FoFs) made investing more disciplined, diversified, and cost-effective for retail participants. Regulatory refinements continued, with standardized disclosures, limits on expense ratios (TERs), and the removal of entry loads improving investor protection and reducing costs. Focused investor education initiatives and simplified Know Your Customer (KYC) procedures also played a vital role in increasing awareness and participation. These initiatives resulted in the industry’s Assets Under Management (AUM) crossing the Rs. 10 lakh crore mark by the end of 2014.

Phase 2: Accelerating Growth and Access (2015 – March 2025)

The period from 2015 onwards marked an era of accelerated expansion and democratization. Industry AUM experienced nearly six-fold growth, reaching over Rs. 53.40 lakh crore by March 2024, before climbing further to Rs. 65.74 lakh crore by March 2025. India’s share of the global mutual fund market has also witnessed a substantial increase. The emphasis during this phase was on removing the barriers that hindered wider acceptance:

- Overcoming Hurdles:

-

- For Cautious Investors: Addressing concerns about market volatility and building trust, while demonstrating value compared to guaranteed return products like PPF. Managing the impact of expense ratios was also key.

- For Aware but Hesitant Investors: Improving the reach and accessibility of distribution networks, particularly beyond major cities, to provide necessary guidance and build confidence for self-directed investing.

- For New Investors: Tackling low financial literacy, especially in smaller towns, countering the strong preference for traditional assets, and simplifying the understanding of mutual fund products.

- Catalytic Interventions:

- Products & Strategies: SIPs became a cornerstone, mitigating volatility concerns and promoting disciplined, affordable investing. Direct plans and passive instruments (Index Funds, ETFs) offered lower-cost alternatives.

- Technological Integration: Digital platforms transformed the investment experience, offering seamless onboarding (e-KYC, Aadhaar, UPI), portfolio tracking, and goal-based planning. Registrars and Transfer Agents (RTAs) provided the essential back-end infrastructure for scale, efficiency, and transparency, including platforms like MF Central for service requests.

-

- Industry Initiatives: Through multiple campaigns, perceptions were changed, and SIPs were actively promoted. Numerous Investor Awareness Programmes (IAPs) were conducted.

-

- Regulatory Support: SEBI’s actions were pivotal, including rationalizing scheme categories for better understanding, capping TERs to enhance returns, mandating ESG disclosures, refining hybrid fund rules, and using incentives to encourage growth in smaller (B30) cities. Risk management frameworks and transparency norms were continuously strengthened.

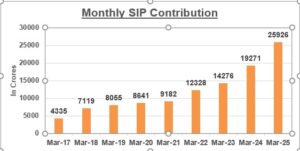

These combined efforts resulted in substantial growth across metrics – AUM, no of folios (hitting 23.45 crore by March 2025), and SIP inflows (Rs. 25,926 crore during March 2025). The industry increasingly adopted a philosophy centered on investor needs.

Drivers of Growth: The Engine of Expansion

The impressive expansion of India’s asset management sector is attributable to a confluence of powerful drivers:

1. Economic Prosperity: Sustained high GDP growth forms the bedrock, increasing disposable incomes and the capacity for household savings and investment.

2. Shift to Financial Assets: Households are gradually allocating more savings towards financial instruments over physical assets. Mutual funds are capturing an increasing share of these financial savings, gaining favor over traditional investment options, particularly in search of higher returns.

3. The SIP Phenomenon: SIPs have revolutionized participation. Their structure promotes discipline, mitigates timing risk through cost averaging, and makes market entry accessible via small, regular investments. SIP AUM and monthly inflows have shown remarkable, consistent growth, demonstrating investor commitment even through market fluctuations. By 2025, monthly SIP inflows had surpassed Rs. 25,000 crore, involving over 5 crore investors. Domestic investors, largely through SIPs, have become a stabilizing force in the market.

4. Digital Revolution: Technology has dramatically lowered barriers:

- Accessibility: Online platforms (from fintechs, AMCs, distributors) offer unprecedented ease of access for investing, tracking, and managing portfolios. Functionalities such as digital KYC and UPI payments have simplified procedures. Digital channels accounted for nearly 90% of purchase transactions in FY25.

- Efficiency: Scalable infrastructure provided by RTAs and platforms like MF Central improve operational efficiency and transparency. The widespread availability of smart phones and affordable internet fuels this digital uptake.

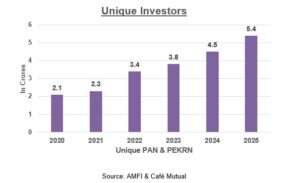

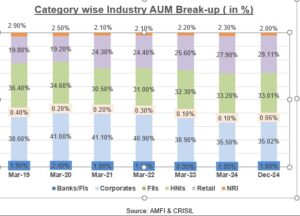

5. Rising Share of Retail Participation: Retail investors have significantly expanded their presence in the total AUM landscape, with their allocation climbing from 19.80% in 2019 to 28.11% by Dec-24. This upward trajectory clearly demonstrates enhanced awareness of and greater access to this investment avenue. Proactive and sustained efforts by the industry, including comprehensive campaigns and educational initiatives, have been instrumental in empowering retail investors. This empowerment has, in turn, fostered more informed investment choices and bolstered their capacity to navigate market volatility effectively.

6. Enabling Regulatory Environment: SEBI’s consistent focus on transparency, investor protection, product simplification, and fair practices has built significant trust in the mutual fund structure. Measures like TER caps and clear scheme categorization have directly benefited investors.

7. Distribution Expansion: Growth in the network of distributors and advisors, including RIAs, has improved reach and provided crucial guidance, particularly for first-time investors.

8. Product Diversification & Passive Appeal: A wide array of fund types caters to diverse investor profiles. The rapid rise of passive funds (Index Funds, ETFs) stands out, driven by their inherent low cost, simplicity, transparency, and strong performance relative to benchmarks, especially in certain segments like large-cap equity. Institutional mandates (like EPFO investing in ETFs) have also boosted passive AUM.

9. Favorable Demographics: India’s large, young population is generally more comfortable with technology and market-linked investments compared to previous generations.

Prevailing Headwinds: Challenges on the Horizon

Despite its dynamism, the Indian asset management industry confronts significant challenges that need addressing to unlock its full potential:

1. Market Depth: Penetration levels remain low by international comparison. A vast segment of the population, particularly beyond the major cities, is yet to participate in mutual funds. Despite increasing, the AUM-to-GDP ratio trails international standards.

2. Financial Awareness: Insufficient understanding of financial products, risk-return trade-offs, and market mechanisms continue to be a barrier, especially in Tier-2/3 cities and rural India.

3. Traditional Investment Mindset: Deep-seated preferences for physical assets and guaranteed-return products stemming from cultural factors and perceived safety hinder faster adoption of market-linked schemes.

4. Distribution Gaps: Ensuring effective advice and access in less penetrated regions remains a challenge. While digital access helps, the need for human guidance, especially for novice investors, requires a more extensive and skilled distribution network.

5. Building and Maintaining Trust: Amidst inherent market volatility, consistently building investor trust through transparency, fair practices, and effective communication is paramount. Product complexity can also be a deterrent.

6. Cost Pressures: The shift towards low-margin passive funds creates fee compression for AMCs, particularly those reliant on active management fees. Simultaneously, costs associated with regulatory compliance, technology upgrades, and enhancing cyber security are rising. Balancing these requires a strong focus on operational efficiency.

7. Navigating Market Volatility: Managing portfolios effectively during periods of market stress (like the drop seen in early 2025) to deliver consistent returns and retain investor confidence is an ongoing challenge. Protecting smaller investors during such times is a key responsibility.

8. ESG Integration and Climate Risk: The industry faces criticism for lagging in meaningful integration of Environmental, Social, and Governance (ESG) factors and climate risk assessment. Many AMCs have low climate preparedness scores, limited disclosure (especially on financed emissions), and continue significant exposure to high-emitting sectors, potentially posing risks to investors and hindering alignment with national sustainability goals.

9. Demand for Personalization: Investors increasingly expect tailored solutions and advice, requiring AMCs to invest in data analytics and sophisticated advisory capabilities beyond standardized products.

The Way Ahead: Guiding Towards Financial Wellbeing

Looking towards 2047, the Indian asset management industry aims to transition from facilitating financial inclusion to actively fostering financial wellbeing for all citizens. This entails empowering individuals with the control, resilience, goal-orientation, and autonomy needed for a secure financial life. Achieving this ambitious vision requires strategic focus on several key areas:

1. Accelerating Penetration: The industry aspires to significantly boost participation, potentially reaching 15% of the population by 2047, driving AUM towards projections like USD 33 trillion and an AUM-to-GDP ratio exceeding 100%. Realizing this goal necessitates intensified efforts in B30 cities and rural areas.

2. Prioritizing the Investor: A fundamental shift towards an investor-centric model is essential, designing solutions and communication strategies that resonate with the diverse financial realities, cultural contexts, and behavioral patterns across India.

3. Enhancing Simplicity and Access: Continuously refining digital platforms for ease of use, incorporating vernacular languages, and simplifying financial terminology are crucial. Exploring offline or hybrid models for low-connectivity areas and further streamlining on boarding processes remain important.

4. Innovating Relevant Products: Creating investment solutions tailored to life stages (e.g., retirement SWPs, education savings plans), specific goals, cultural preferences, and emerging trends (like ESG or thematic investing) will broaden appeal. Technology can enable dynamic risk management and potentially tokenize traditional assets.

5. Championing Inclusivity: Proactively designing accessible platforms (e.g., for visually impaired users) and flexible products (e.g., for gig workers) is necessary. Utilizing visual and audio communication aids can reach individuals with limited literacy.

6. Driving Behavioral Change: Employing insights from behavioral finance to nudge positive investment habits, building trust through transparent communication and community outreach, and embedding financial literacy from an early age are key levers.

7. Strengthening Last-Mile Delivery: Expanding reach through a ‘phygital’ approach – combining digital tools with physical touch points. This involves empowering local intermediaries and leveraging existing community networks (like post offices or CSCs) for guidance and on boarding.

8.Fostering Ecosystem Synergy: It is vital that the efforts of regulators, AMCs, distributors, and technology providers should be aligned towards common goals like standardized processes, localized awareness campaigns, and investor-centric policy advocacy.

9. Evolving Regulatory Landscape: Continued collaboration with SEBI is essential to adapt regulations that support innovation while safeguarding investors. Recent regulatory actions focus on faster fund deployment from New Fund Offers (NFOs), mandatory employee co-investment in schemes, disclosure of stress test results, and facilitating passive investing through frameworks like MF Lite. Addressing gaps in climate risk disclosure and management is also becoming critical.

10. Leveraging Technology: Fully harnessing the potential of AI, big data, cloud computing, and India’s digital public infrastructure (like UPI, ONDC, Account Aggregator) will be key to enhancing personalization, operational efficiency, risk management, and overall reach.

Conclusion: Forging an Empowered Financial Future

India’s asset management sector, led by its burgeoning mutual fund industry, has matured significantly, becoming a vital conduit for channeling savings into productive investments and empowering citizens financially. Fueled by a potent mix of economic growth, demographic shifts, technological advancements, regulatory foresight, and increasing investor sophistication, the industry has achieved remarkable scale, with AUM poised to cross the Rs. 100 lakh crore threshold. Domestic investors, particularly through the disciplined route of SIPs, are now a formidable force shaping market dynamics.

However, the mission extends beyond mere asset accumulation. The industry faces the ongoing tasks of deepening penetration into underserved segments, simplifying complexities, navigating market uncertainties responsibly, and addressing emerging concerns like climate risk integration. The ultimate goal is to transition from providing access to fostering genuine financial wellbeing across the nation.

The path towards 2047 requires unwavering commitment to investor-centricity, innovation tailored to India’s unique context, and collaborative efforts across the entire ecosystem. By focusing on simplicity, relevance, inclusivity, and leveraging the country’s digital prowess, the industry can overcome existing challenges. The vision is clear: to provide financial security and prosperity for every Indian household, thereby contributing significantly to the nation’s broader economic aspirations and setting a global example for inclusive wealth creation.

Written by:

Ritesh Kumar Binani

Research Officer

State Bank Academy

Gurgaon

“Views and Opinions expressed in the article are mine and not of the Bank’’