GREEN BANKING : CHALLENGES & OPPORTUNITIES

Abstract:

The Banking industry plays an important role in economic growth and environmental protection by promoting environmentally sustainable and socially responsible institutions. The banking of this kind can be termed as “Green Banking”. Change is the need of the hour for survival in all spheres. Banks can provide important leadership for the required economic innovation that will provide new opportunities for financing and investment policies. Green Banking means combining operational improvements, technologies and changing client habits in banking business. Adoption of Green Banking practices will not only be useful for environment, but also benefit in greater operational efficiencies, a lower vulnerability to manual errors,fraud, and cost reductions in banking activities. This paper has made an attempt to highlight the major services, challenges, opportunities, strategies of Green Banks in India.

Keywords: Environment protection, global warming, Green banking financial products,& sustainable development.

Introduction:

Environment sustainability is the design and provision of products and services that incorporate and promote waste minimization, effective use and reuse of resources. Its aim is to protect the environment for the benefit of current and future generations. It is all about meeting

- Research Supervisor, Department of Business Administration, Yogi Vemana University, Kadapa, Andhra Pradesh.

- Research Scholar, Department of Business Administration, Yogi Vemana University, Kadapa, Andhra Pradesh. E-mail: [email protected].

- Research Scholar, Department of Business Administration, Yogi Vemana University, Kadapa, Andhra Pradesh.

needs and seeking a balance between people, the environment and the economy. According to the United Nations, sustainable development meets the needs of the present without compromising the ability of future generations to meet their own needs. Sustainable development

and preservation of environment are now recognized globally as overriding imperatives to protect our planet from the ravages inflicted on it by mankind. Various global initiatives are underway to counter the ill-effects of development that we encounter today such as carbon foot print, global warming, climate change, fickle weather, floods, droughts, pollution, high greenhouse gas emissions, etc., while still there is no consensus among the countries onsharing the burden of ecological footprint, most of the countries have been taking aggressive measures to tackle global warming and climate change.

The banking industry influences both economic growth and development, both in terms of quality and quantity, leading to a change in the nature of economic growth. Therefore, banking sector plays a crucial role in promoting environmentally sustainable and socially responsible investment. Banks may not be the polluters themselves but they usually have a banking relationship with some companies/investment projects that are polluters or could be in future.Banks also contribute to ecological footprint directly and indirectly through investment/lending in their customer enterprises. As such they need to play a key role in optimizing /reducing the carbon footprint. It is said that what is not measured, is notmanaged.

Concepts of Green Banking:

Green banking means promoting environment friendly practices and reducing carbon footprint from banking activities. This comes in many forms viz., using online banking instead of branch banking, paying bills online instead of mailing them, opening of commercial deposits and money market accounts in online banks etc.,

Green banking refers to the efficient and effective use of computers, printers and servers to optimize the use of energy and waste-less paper. One of the important ways in which banks can implement green banking is by promoting the use of online banking among customers. Online banking helps reduce paperwork and the need to travel to bank branches. This positively impacts the environment. This facility is beneficial for banks, as it reduces operational costs and increases efficiency.

This concept of “Green Banking” would be mutually beneficial to the banks, industries and the economy. Green banking will also ensure the greening of the industries but it will also facilitate in improving the asset quality of the banks in future.

Carbon footprint is a measure of an organization’s or entity’s impact on the environment in terms of the amount of greenhouse gases produced, measured in units of carbon dioxide equivalent. Global warming is a measure of rising average temperature of Earth’s atmosphere and oceans and its projected continuation. In the last 100 years, the Earth’s average surface temperature increased by about 0.80C (1.4 F) with about two-thirds of the increase occurring over in the last three decades. Most global warming is caused by increasing concentrations of greenhouse gases produced by human activities such as deforestation and burning fossil fuels.Climate change is the change in temperature and weather patterns due to certain human activity like burning fossil fuels. The changes include global average air and ocean temperature, widespread melting of snow and ice and rising global sea levels. Therefore, a common thread running across all these initiatives is the focus on reducing the demand for fossil fuels by implementing the 3R’s viz. Reduce, Reuse and Recycle.

Characteristics& features of Green Banking:

Depending on the state, a green bank may conform to a variety of forms, utilize many different public funds, and create a diverse array of financial products. Banks may utilize financial tools such as long-term and low interest rate loans, revolving loan funds, insurance products and low-cost public investments or it may design new financial products. Ultimately, all green banks will exhibit several common characteristics:

- Stimulate demand by covering 100% of the upfront costs with a mixture of public and private financing.

- Leverage public funds by attracting much greater private investment for clean energy and markets.

- Recycle public capital so as to expand green investment and leave taxpayers unharmed.

- Scale-up clean energy solutions as fast as possible, maximizing clean electricity and efficiency gains.

Evolution of Green Bank:

First Green Banking was founded in 2009 in the state of Florida. Based in Eustis and Clermont, Florida, USA, First Green Banking is a customer-driven community bank providing personalized service,localized decision- making and proven technology by promoting a positive environment that is acceptable to the community.

State Bank of India, India’s largest commercial bank, took the lead in setting high sustainability standards and completed the first step in its ‘Green Banking’ initiative with Shri O.P.Bhatt, Chairman, SBIinaugurating the bank’s first Wind farm project in Coimbatore. Recent Green Banking initiatives include a push for solar powered ATM’S , paper less banking for customers, clean energy projects and the building of Wind mills in rural India. SBI is a leader in Green Banking.

Green Banking Financial Products:

Green banking helps to create effective and far-reaching market-based solutions to address a range of environmental problems, including climate change, deforestation, air quality issues and biodiversity loss, while at the same time identifying and securing that benefit customers. Some of Green banking financial products includes: Green mortgages, online banking, remote deposit capture, green car loans and green credit cards.

- Green Mortgages:In general Green mortgages also known as Energy Efficient Mortgages(EEM’S), provide retail customers with considerably low interest rates compare market rates for clients who purchase new energy efficient homes or invest in retrofits, energy efficient appliances or green power. Banks can also choose to provide green mortgages by covering the cost of switching a house from conventional to green power, as well as include this customer benefit when marketing the product.

- Online Banking: Online banking, also known as internet banking, e-banking or virtual banking, is an electronic payment system that enables customers of a bank or other financial institution to conduct a range of financial transactions through the financial institution’s website.

- Remote Deposit Capture: Remote deposit capture (RDC) is a system that allows a customer to scan cheques remotely and transmit the cheques images to a bank for deposit, usually via an encrypted Internet connection. When the bank receives a cheque image from the customer, it posts the deposit to the customer’s account and makes the funds available based upon the customer’s particular availability schedule. Banks typically offer Remote Deposit Capture to business customers rather than to individuals.

- Green Car Loans: Many green car loans encourage the purchase of cars for below market interest rates, which demonstrate higher fuel efficiency.

- Green Credit Cards:A green credit card allows cardholders to earn rewards or points which can be redeemed for contributions to eco-friendly charitable organizations. These cards offer an excellent incentive for consumers to use their green card for their expensive purchases.

Green Banking opportunities:

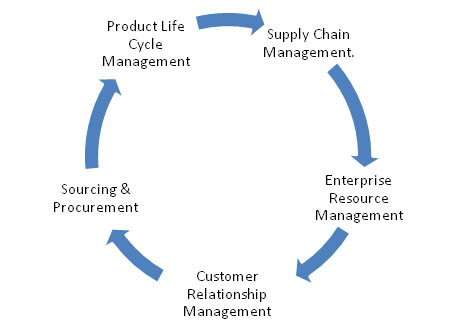

A Green Bank requires each of its functional units and activities to be Green- environmentally friendly and help to improve environmental sustainability. Several opportunities are available for banks to go green their functional units and activities. Key among them are:

- Supply Chain Management(SCM)

SCM is the management of the flow of goods and services.It includes the movement and storage of raw materials, work-in-process inventory, and finished goods from point –of- origin to point- of-consumption. Interconnected or interlinked networks, channels and node businesses are involved in the provision of products and services required by end customers in a supply chain.

- Adopt techniques and plans to minimize inventory and wasted freight.

- Adopt networked design using a carbon foot print.

- Enterprise Resource Management(ERP)

ERP is a category of business-management software, typically a suite of integrated applications that an organization can use to collect, store, manage and interpret data from many business activities, including product planning, purchase, manufacturing or service delivery ,marketing and sales, inventory management, shipping and payment.

- It facilitates paper less transactions.

- Adopt techniques for workforce and parts optimization as well as intelligent device management.

- Customer Relationship Management(CRM)

Customer relationship management is an approach to managing a company’s interaction with current and future customers. It tries to analyze data about customers history with a company, to improve business relationships with customers, specifically focusing on customer retention, and ultimately to drive sales growth.

One important aspect of the CRM approach is the systems of CRM that compile information from a range of different communication channels including a company’s website, telephone, email, live chat, marketing materials, social media, and more. Through the CRM approach and the systems used to facilitate CRM, businesses learn more about their target audiences and how to best cater to their needs.

- Sourcing & Procurement:

In business, the term sourcing refers to a number of procurement practices, aimed at finding, evaluating and engaging suppliers for acquiring goods and services. Outsourcing is the process of contracting a business function to someone else., select vendors for sustainability rating for their products, services and operations.

- Product Life Cycle Management:

In industry,PLC is the process of managing the entire lifecycle of a product from inception, through engineering design and manufacture, to service and disposal of manufactured products.

- Design and offer banking products & services in such a way that consume less resources and energy and thereby reduce carbon foot print.

- Implement effective systems for product end- of- life management that have minimal impact on environment.

Green Banking Services

Banks are developing new products and services that respond to customers demand for sustainable choices. Following are some of the options that banks should offer to their customers:

- Electronic and mobile banking facilitates customers to perform most of their bank needs anytime, anywhere.

- Automatic payments reduce the need to write and send cheques by mail.

- Paperless statements, product information guides and annual reports to customers and stakeholders.

- Offering and promoting mutual funds that focus investment in ‘Green’ companies.

- Credit cards and debit cards can be used while making the payment of various expenses without carrying money.

- Mobile banking is used for performing balance cheques, account transactions, payments, credit appliances etc., via mobile phone or Personal Digital Assistant (PDA).

Challenges of Green Banking

While adopting green banking practices, the banks would face the following challenges:

- Reputational Risk: If banks are involved in those projects which are damaging the environment they are prone lose their reputation. There are few cases where environmental management system has resulted in cost saving, increase in bond value.

- Diversification Problem: Green banks restrict their business transaction to those business entities who qualify screening process done by green banks. With limited number of customers they will have a smaller base to support them.

- Start-up face: Many banks in green business are very new and are in start-up face. Generally it takes 3 to4 years for a bank to start making money. Thus it does not help banks during recession.

- Credit Risk: Credit risk arises due to lending to those customers whose businesses areeffected by the cost of pollution, change in environmental regulation and new requirements of emission level.

- High operating cost: Green bank requires talented and experienced staff to provide proper services to customers. Experienced loan officers are needed, they give additional experience in dealing with green business and customers.

Green Banking Strategies

According to MdShafiqul and Prahalled (2013), green banking activities involve two major approaches i.e., green transformation of internal operation and environmentally responsible financing.

- Green Banking through internal operations: It means all bank should adopt green banking activities in their day to day operations. These include adopting appropriate ways to use renewable energy, automation and minimizing their carbon footprint. In the past few years, all the banks have incorporated paperless technologies in their internal operations to help the environment as well as provide their customers efficient and better services. In their day-to-day business operations, banks ordinarily generate carbon emissions through the usage of paper, electricity, stationary, lighting, air conditioning and electronic equipment. Green banking internal operations include on line account opening, online banking, mobile banking, net banking, electronic fund transfer as well as the use of ATM, cash and cheque deposit machines, credit and debit cards, e-statement SMS alert, mini image statement etc.

- Green Finance: Green Finance refers to banks that provide financial assistance to environmentally responsible projects. The purpose is to provide financial assistance to green technology and pollution reduction projects to reduce external carbon emissions. The bank support industries that are resource efficient and emit low carbon footprint. Priority is given to financing eco-friendly business activities and energy efficient industries such as waste water treatment plant, waste disposal plants, bio-gas plants, renewable energy projects, hybrid car projects and so on.

Environmental Management by Banking Institutions

- Now a days, most of the commercial lending process in different parts of the world scrutinizes projects with a set of tools by incorporating environmental concerns in their day-to-day business. The financial institutions should encourage projects which take care of the following aspects while financing them.

- There should be an Environmental Impact Assessment (EIA) of each project recommending the measures needed to prevent, minimize and mitigate the environmental negative impact before financing the projects.

- While investing or funding the projects, the financial institutions should assess the sensitive issues like vulnerable groups; involuntary displacement etc and projects should be evaluated in terms of environmentally important areas including wetlands, forests, grasslands and other natural habitats.

- Banking institutions need to evaluate the value of real property and the potential environmental liability associated with the real property. Therefore, the banks should have right to inspect the property or to have an environmental audit performed through the life of the loan.

- Banks also need to monitor post transaction for the ideal environmental risk management program during the project implementation and operation. There should be physical inspections of production, resources, training and support, environmental liability, audit programs etc.

- The next round of evaluation includes loan structuring, credit approval, and credit review and loan management. Further banks have annual audits, quarterly environmental compliance certificate from the independent third party and also from the government.

- Further the banks can introduce green bank loans and products like:

- Investing in projects related to recycling, farming, waste disposal through reduced interest rates on loans to home owners for installing a solar energy system.

- Providing option for customers to invest in environmentally friendly bankingproducts.

- Investing in resources that combine ecological concerns and social concerns.

Measures to encouraging Green Banking:

Banks are responsible corporate citizens. Banks believe that every small “GREEN” step taken today would go a long way in building a greener future and that each one of them can work towards better global environment. The purpose is to provide cost efficient automated channels and to build awareness and consciousness of environment, nation and society. Green banking is really a good way for people to get more awareness about global warming; each businessman will contribute a lot to the environment and make this earth a better place to live. Until a few years ago, most traditional banks did not practice green banking or actively seek investment opportunities in environmentally-friendly sectors or businesses. Only recently have these strategies become more prevalent, not only among smaller alternative and cooperative banks, but also among diversified financial service providers, asset management firms and insurance companies.

- Educate through the bank’s intranet and public websites.

- Construct a website and spread the news.

- Participate in events and communicate through press.

- Setup outlets to promote Green business.

- Carbon foot print reduction by mass transportation and energy consciousness.

- Impart education through E- learning programs.

Conclusion:

Possible policy measures and initiative to promote green banking in India has become the need of the hour. In a rapidly changing market economy where globalization of markets has intensified the competition, banks should play a pro-active role to take environmental and ecological initiatives. The banking and financial sector should be made to work for sustainable development. As far as green banking is concerned, Indian banks are running behind time and it is the need of the hour to think it seriously for the sustainable growth of the nation.Green Banking concept will be beneficial for both the bankingindustries and the economy. Not only “Green Banking” will ensure the greening of the industries but it will also facilitate in improving the asset quality of the banks in future.

Authors

Dr. A. Amruth Prasad Reddy

M.B.S.Sravanthi

Shaik Rehana Bhanu

References:

- Green Banking: An IDRBT publication August 2013.

- https://www.firstgreenbank.com/about/our-story accessed 3rd July 2016.

- http://www.coalitionforgreencapital.com/whats-a-green-bank.html accessed 3rd July 2016.

- , “The role of Green Banking in sustainable growth,” International Journal of Marketing, Financial services and Management Research, vol.no.2, February 2012, pp.28,34.

- Ashis Kumar Chaurasia., “Green Banking practices in Indian Banks,” Journal of Blue Square Publishing House, vol.no.1, Issue 1,February 2014,pp. 43-53.

- Saleena T.A., “Go Green: Banking sector perspective,” Abhinav National monthly preferred Journal of Research in Commerce & Management, vol.no.3, Issue 11, November 2014, pp. 28-31.

- http://www.aelp.org.uk/supply/details/supply-chain-management-guide/, published 2013, accessed 31 March 2015

- Shaw, Robert (1991). Computer Aided Marketing & Selling. Butterworth Heinemann.ISBN 978-0-7506-1707-9.

- “About PLM,” CIMdata, Retrieved 4th July 2016.

- “What is PLM,” PLM Technology Guide, Retrieved 4th July 2016.