Banking – The Future of Customer Experience AI-Powered Hyper-Personalized

Introduction

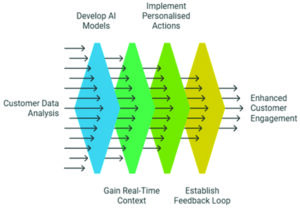

Banking, for most of the 20th century, operated on the principle of uniformity, standard products, standard pricing, standard service. Everyone with similar income profiles or occupations received roughly the same treatment. But the digital revolution shattered this sameness. With data now flowing from transactions, devices, digital interactions, and online behavior, banks began seeing customers not as segments, but as individuals with unique financial patterns and needs. And at the heart of this transformation sits AI-powered hyper-personalisation, a paradigm that seeks to understand customers at a “segment of one.”

As a global financial CEO remarked recently, “Personalisation will not be the differentiator; it will be the minimum expectation.” Customers today want banks that anticipate their needs, understand their life journeys, offer tailored advice, and create meaningful digital experiences. AI is what makes this possible turning millions of data points into deep insights and real-time decisions. Hyper-personalisation is not a marketing tactic anymore; it is a complete redesign of customer experience.

What Is Hyper-Personalized Banking?

At its core, hyper-personalization means the ability to use real-time data, behavioral signals, and AI models to design financial experiences that are tailored to each customer’s unique context. Unlike traditional personalization (such as sending a birthday message or segment-based offer), hyper-personalization uses:

- Continuous behavioral analysis

- Real-time contextual triggers

- Predictive modelling

- Recommendation engines

- Conversational AI

As a result, banks can anticipate what a customer might do next, or might need next, even before the customer initiates contact. Hyper-personalized banking goes beyond preferences, it taps into intent, habits, life-stage indicators, and micro-behaviors.

Why AI Drives Personalisation to the Next Level

Artificial Intelligence is what makes deep personalisation scalable. AI systems analyze thousands of variables in seconds, identify patterns invisible to humans, and generate personalized actions for millions of customers simultaneously. Four powerful capabilities make AI the engine of hyper-personalized banking:

Predictive Intelligence

- AI predicts upcoming needs, buying a home, investing surplus income, planning insurance, paying school fees, or managing a short-term liquidity crunch.

Real-Time Decisioning

- Banks can offer dynamic credit limits, personalized pricing, tailored product suggestions, and real-time alerts based on immediate behavior or context.

Behavioral Understanding

- AI detects spending habits, savings discipline, risk appetite, and financial stress signals more accurately than questionnaires or surveys.

Scalable Personalisation

- What a relationship manager can do for 100 customers, AI can do for 10 million with consistency and speed.

This technological leap is why McKinsey estimates that AI-led personalisation can increase revenue from personalized services by 30% to 40% in banking.

Real-Time Personalized Offers and Smart Credit Decisions

Hyper-personalized banking becomes most visible in lending. With the help of AI, banks can now deliver extremely context-aware offers:

- A customer browsing travel portals may instantly receive a personalized travel loan or credit card upgrade.

- An MSME that shows higher digital receipts may get a pre-approved working capital increase.

- A salaried worker nearing month-end may receive a savings reminder, or an interest-free overdraft suggestion.

These are not random promotions, they are intent-driven interventions. Studies suggest that personalized offers achieve 3–5x higher response rates, while reducing acquisition costs by up to 25%.

More importantly, AI transforms credit risk models. Instead of relying only on historical data, AI-based behavioral underwriting considers:

- Spending consistency

- Income volatility

- Digital footprints

- Device behavior

- Repayment timing patterns

This makes underwriting sharper, more inclusive, and more tailored. For new-to-credit customers who lack traditional credit histories, AI-driven personalisation has reduced default rates by 20–30% in several pilot studies across Asia.

AI as a Financial Mentor: Personalized Wealth and Wellness

AI-powered hyper-personalisation is reshaping wealth management, traditionally a service reserved for high-net-worth individuals. Today, even mass retail customers can access:

- Personalized investment portfolios

- Goal-based planning

- Tax-optimized recommendations

- Nudges to improve savings discipline

- Predictive retirement projections

AI becomes a 24×7 financial coach, guiding customers through simple decisions (budgeting, savings targets) and complex ones (tax planning, portfolio diversification). Surveys show that 70% of millennials prefer automated, tailored financial guidance over traditional advisory channels.

As wealth creation expands in India and other emerging markets, AI-powered personalisation will become a key differentiator for banks.

Conversational AI: The Humanized Banking Assistant

With the rise of GenAI, conversational banking has moved far beyond simple FAQs. AI-driven chatbots and voice assistants now handle personalized tasks such as:

- Financial summaries tailored to weekly or monthly habits

- Smart categorization of spending

- Personalized action steps to reduce fees or charges

- Recommendations for bill payments, UPI limits, or investments

The best conversational AIs are context-aware, they remember previous interactions, detect emotional tone, and adapt responses accordingly. Banks using advanced conversational AI report:

- 60% faster query resolution

- Higher customer satisfaction

- Up to 30% reduction in contact Centre load

Hyper-personalisation is no longer limited to products; it is embedded in everyday service interactions.

Life Event Prediction: Banking Ahead of Need

One of the most powerful aspects of AI is its ability to detect upcoming life events. For example:

- An increase in pharmacy expenses and hospital searches may indicate upcoming medical needs.

- Regular browsing of education portals could signal planning for higher studies.

- Consistent savings with rising rent expenditure may suggest an upcoming home purchase.

- Salary inconsistencies may signal job transition or income stress.

These signals allow banks to anticipate needs before customers voice them. A timely message such as “We can help you plan your child’s education” can be more valuable than a generic promotion.

This is what makes hyper-personalisation empathetic, not just intelligent.

Personalized Fraud Detection and Security

AI not only enhances customer convenience it also enhances safety. Hyper-personalized security systems use behavioral biometrics such as:

- Typing rhythm

- Device handling patterns

- Navigation style in the app

- Typical spending patterns

- Location consistency

If the behavior deviates from a customer’s normal pattern, AI immediately flags suspicious activity. Global studies show that personalized security reduces fraud losses by 20–35%, making it both effective and customer-friendly.

Ethical and Responsible Personalisation

With great personalisation comes great responsibility. Hyper-personalisation relies on extensive data, making responsible AI essential. Banks must ensure:

- Transparent customer consent

- Bias-free algorithms

- Clear data protection policies

- Explainable AI decisions

- No discriminatory outcomes

Regulators are emphasizing fairness and transparency in AI use. As the Financial Stability Board cautions, “AI must strengthen, not undermine, customer trust.” A personalized banking model without ethical safeguards can compromise long-term trust. Hence, responsible personalisation will determine the sustainability of this trend.

What the Future of Hyper-Personalized Banking Looks Like

By 2030, hyper-personalized banking will look significantly different from today:

- Every customer will have an AI-powered financial twin guiding spending, saving, investing, and borrowing.

- Credit limits, interest rates, and loan terms will be dynamically priced based on real-time behavior.

- Branch staff will use AI-driven dashboards to understand customer needs before interaction begins.

- Personalized financial wellness scores will become common, as normal as credit scores today.

- Banks will shift from reactive service (“How can I help?”) to proactive service (“You may need this next”).

- Complaints will drop as AI identifies issues and resolves them before customers report them.

The true promise of hyper-personalisation is not just convenience, it is confidence, empowerment, and trust.

Conclusion

AI-powered hyper-personalized banking marks the beginning of a new era, one where customers are not treated as account numbers, but as individuals with unique journeys. It replaces standardized templates with contextual intelligence, generic advice with tailored guidance, and reactive service with predictive insight.

As Satya Nadella observed, “AI doesn’t replace human intelligence; it amplifies it.” In banking, it amplifies empathy, foresight, and the ability to serve with precision. The banks that embrace hyper-personalisation will emerge as trusted partners in people’s financial lives, guiding them, protecting them, and empowering them.

The future of customer experience in banking will not simply be digital, it will be deeply personal, intelligently human, and powered by AI.

Authored by:

Amit Kumar

Chief Manager Faculty

SBILD Bhavnagar