From Risk Control to Risk Intelligence: The Future of Risk Management in Indian Banking in a Digital & AI-Driven World

Introduction

Indian banking is undergoing a silent transformation, one that is not visible in balance sheets alone but is deeply ingrained in algorithms, data streams, and digital footprints. Every second, millions of financial decisions are being made across the country from a small UPI payment in a rural village to large corporate credit disbursements in metropolitan hubs. This unprecedented scale of activity has redefined the very nature of risk.

Today, Indian financial system processes over 100 billion digital transactions annually, with UPI alone handling transactions worth more than Rs. 18 lakh crore per month. Simultaneously, the banking system has achieved a significant milestone by reducing gross NPAs to nearly 3%, even as credit growth continues in double digits. While these indicators reflect strength and stability, they also mask a more complex reality, the increased underlying risks associated with it. Today, risk is no longer confined to credit defaults or market volatility; it is now dynamic, interconnected, and often invisible.

Traditional risk management strategies, which are mostly reactive, compartmentalized, and compliance-driven, are becoming less and less effective in this rapidly changing ecosystem. The rules of the game have been drastically changed by the advent of digital banking platforms, real-time data analytics, and artificial intelligence. These days, risks appear in milliseconds, spread across systems instantaneously, and require equally quick and clever answers.

A new paradigm is required in light of this change, one in which risk management is about anticipating, adaptability, and strategic enablement rather than just mitigation. Banks must transition from hindsight-driven controls to foresight-driven intelligence, using data and technology to manage uncertainty and turn it into an opportunity.

The future of Indian banking will essentially rest on how well risks are recognized, quantified, and managed in a world that is becoming more digital and AI-driven rather than how well they are avoided.

The Changing Risk Landscape in Indian Banking

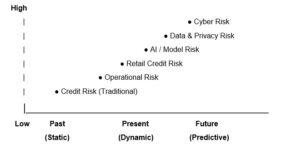

As illustrated in chart 1, the risk architecture of Indian banks is fundamentally changing from linear, predictable risks to dynamic, linked uncertainty.

Once restricted to credit and market hazards, it now encompasses a wider range molded by global interconnectedness, data proliferation, and digitalization. Three key factors—scale, speed, and sophistication are driving this change. Let us understand today’s risk environment in Indian Banks.

1. Digital Explosion and Real-Time Risk

The pace of risk transmission has been greatly accelerated by India’s leadership in digital payments, with UPI transactions surpassing Rs. 18 lakh crore per month. These days, banking operates in a real-time, round-the-clock environment where hazards arise and intensify rapidly.

Important issues include:

- Quick spread of fraud between accounts

- Technology outages’ effects on the entire system

- Verification time is limited because instant transactions are anticipated.

Risk is now continuous rather than episodic, necessitating real-time reaction and monitoring systems.

2. Retail Credit Growth and New-Age Lending Risks

Retail credit now forms nearly 30–35% of total advances, driven by digital lending and fintech partnerships. While this supports financial inclusion, it introduces new vulnerabilities:

- Making loans to debtors with less papers and thin files

- Using algorithms for underwriting

- Increasing danger of excessive leverage

- Co-lending and embedded financing provide complex exposures.

As lending becomes more data-driven rather than collateral-based, model accuracy and data quality become more crucial.

3. Cybersecurity as a Core Business Risk

Cyber risk has emerged as one of the most critical threats as digitization has increased. Cases of digital fraud have increased dramatically in recent years due to:

- Phishing and deep fake scams powered by AI

- Ransomware attacks on banking systems

- Third-party integration vulnerabilities

Cyber risks are not only an IT problem; they are a strategic worry due to their global reach, rapid evolution, and unpredictable nature.

4. Data Risk and Privacy Challenges

With the help of technologies like Account Aggregator and Aadhaar, banks now handle enormous amounts of sensitive consumer data. This improves credit evaluation, but it also brings up issues with:

- Data breaches and Unauthorized Access

- Misuse of personal financial information

- Increased Regulatory scrutiny

It is now crucial to strike a balance between data protection and data consumption.

5. Climate and ESG Risks

Climate risk is emerging as a significant factor, particularly for sectors like infrastructure and energy. Banks face:

- Transition risks from policy changes toward sustainability

- Physical risks from climate-related disruptions

- Reputational risks linked to ESG concerns

This necessitates integrating ESG considerations into mainstream risk assessment frameworks.

6. Global and Macroeconomic Uncertainties

Global events are increasingly affecting Indian banks. Asset quality and liquidity can be rapidly impacted by variables like inflation, commodity price volatility, and geopolitical unrest. This interconnectedness calls for scenario-based and forward-looking risk management approaches.

7. Model Risk in the Age of AI

The growing use of AI and machine learning introduces model risk, including:

- Inaccurate predictions under unforeseen conditions

- Lack of transparency in complex algorithms

- Potential biases in automated decision-making

While technology enhances efficiency, over-reliance without adequate oversight can create new vulnerabilities.

Traditional Vs Future Risk Management

The changing risk environment is a structural change rather than just an extension of conventional risks. Today’s risks are more technologically driven, faster, and more interrelated. Banks need to take a comprehensive, enterprise-wide approach as the lines between various risk categories become increasingly hazy. The real challenge is not only controlling risk but also anticipating it and reacting to it quickly and intelligently.

| Aspect | Traditional | Future Approach |

| Nature | Reactive | Predictive |

| Data | Historical | Real time + Alternative |

| Tools | Manual + Rule based | AI/ML Models |

| Coverage | Credit & Market | Enterprise wide (Cyber, ESG, Model Risk |

| Decision-Making | Periodic | Continuous |

Global Best Practices: Lessons for India

Leading global banks demonstrate how risk management can become a strategic advantage when powered by technology and foresight.

- To assist prevent losses worth billions of dollars every year, JPMorgan Chase has implemented sophisticated AI-driven fraud detection algorithms that evaluate millions of transactions in real time.

- In order to ensure that lending decisions take long-term environmental sustainability and transition risks into consideration, HSBC has integrated climate risk into its credit appraisal procedures.

- In the meantime, DBS Bank has invented completely digital risk dashboards for the entire organization that offer real-time insight across business lines, facilitating quick and well-informed decision-making.

These examples underline a critical insight: technology alone is not the differentiator, its strategic integration into risk frameworks is. For India, the journey must progress from mere adoption of global practices to adaptation within local realities, and ultimately to innovation tailored to its unique scale and diversity.

Authored by:

Dr. Ravindra Shrirang Deshmukh

Chief Manager – Research Officer

Union Learning Academy

Sales and Marketing -Bhopal