Credit Monitoring in Banks

Introduction

With liberalization and globalization and opening up of the economy, Indian banking system has become vulnerable to the spillover and contagion effects. The challenges of increased competition and profitable survival have necessitated maintaining high credit quality and controlling growth of stressed assets. During the last decade in the wake of global slowdown, Indian economy has shown definite symptoms of slowdown and the growth rate has gone down significantly. Therefore, challenge before the banks is dual, that, only good quality assets are added and quality of added assets is maintained. In this context ,proper monitoring of credit in banks has assumed greater significance in the effective management of lending. The success of credit monitoring largely depends on two aspects namely the co-operation of the borrower clients in furnishing the required data and statements to the banks on time and the capacity and knowledge of the credit monitoring authorities to take timely decisions and corrective steps to keep the borrowal accounts in good health. This article discussesabout the need for credit monitoring and corrective steps to be taken at an early stage through the monitoring tools and early warning signals Need for Credit Monitoring:

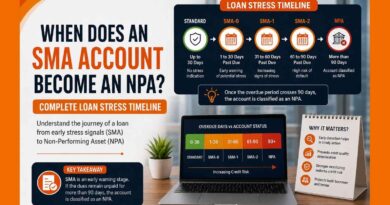

Monitoring of the credit portfolio and individual accounts is essential in order to maintain the quality of the credit portfolio of the bank in a sound condition. In line with the international practices, it is imperative for the banks to implement prudential norms of income recognition and asset classification of the individual borrowing accounts in the credit portfolio.On the basis of the record of recovery of interest and other payables in the borrowal account, the banks classify the accounts as Standard, Sub-standard, Doubtful and Loss Assets. In the event of the borrower not servicing the interest/installment and other payables for a period of maximum 90 days in a term loan account or an overdraft/cash credit and other borrowal accounts remaining out of order for a period of more than 90 days, the account is classified as Sub-standard.Thereafter, depending on the period of default by the borrower and availability of realisable security the relative account is downgraded to doubtful or loss assets. The borrowal accounts in this situation are termed as Non-Performing Assets (NPA).

Objectives of Credit Monitoring

The objectives of credit monitoring are to:

(a) Ensure initial delivery or disbursement of credit after complying with the laid down procedures and conditions with due precautions

(b) Ensure that the credit assets remain in standard category

(c) Endeavour up-gradation of identified weak accounts/watch list accounts and

(d) Take necessary steps to prevent slippage of the accounts to sub-standard and NPA category

Goals ofCredit Monitoring

With the financing of the borrowing units, the banks have a stake in the business of the borrower and, in its own interest, the banker would like to ensure smooth running of the business of the borrower with reasonable growth.This is achieved by ascertaining various monitoring goals for individual assets and these goals are:

(i) Periodical monitoring of the actual performance of the business of the borrower vis-a-vis projections accepted at the time of appraisal of credit facilities. Periodical performance as against the projected level of sales, operating profits, inventory and debt levels, cash flow, etc., have to be obtained and monitored.

(ii) Identifying and evaluating the temporary/critical aberrations coming in the way of smooth functioning of the borrowing unit for timely and suitable action.

(iii) Interacting regularly with the borrowers through timely inspection in order to:

(a) Ascertain the level of sincerity and interest of the promoters in the day-to-day business operations, and to obtain the information regarding production level, inventory level, trend of manufacturing/sales, labour problems, maintenance of production units and other related issues

(b) Ascertain whether the funds invested in the business are adequately protected and whether the day-to-day problems facing the business are being addressed in time

(c) Get a feel of the financial problems of the borrowing unit without delay and to take remedial action on regular or ad hoc basis, after evaluating the same on merit

(d) Ascertain whether there are any impediments in timely service of interest and repayment of installments due to the bank

(e) Ensuring the end use of funds and prevention of diversion of funds and

(f) Ascertain as to whether there is any threat to the recovery of bank’s funds invested in the business and to initiate timely and appropriate recovery measures to protect the interest of the bank

Credit Monitoring Tools :

Safety of the bank’s exposure in credit asset is of paramount importance. The safety is dependent upon risk factors, which are identified and accepted while taking credit exposure. Any event that could result in materialising of these risks into default or even delay in repayment must be diagnosed and identified early.The normal sanction covenants such as maintenance of margin, payment of interest in time, submission of stock statement, submission of other statements by the borrowers, review of accounts at appropriate times, etc., together with the loan-specific stipulations such as raising of the promoter’s contribution, creation of mortgage of a property after completion of the legal formalities, etc., will provide the basic framework to obtain and use various monitoring tools. In this regard, a practicing banker in general and a credit official in particular need to know the objective of monitoring tools, understand their need & relevance and interpret it properly for effective monitoring, for achieving optimum results. It aims to achieve that even within the Standard Asset category, accounts to be persistently upgraded from Special Mention Account (SMA) categories to pure standard category.An exhaustive list of monitoring tools is difficult to be drawn up, as loan- specific issues and factors vary.The following is an inclusive list of various monitoring tools:

1)Certified statement of the actual cost of the project (upon completion) vis-a-vis the original envisaged cost of the project

2) Stock and book-debts statements

3) Monthly Cash Budget, wherever applicable

4) Returns of Quarterly Information System

5) Statements of Monthly Select Operational Data

6) Inspection Reports

7) Stock Inspection Reports of outside agencies.

8) Concurrent/Internal/Revenue/Audit Reports

9) Factory Visit Reports

10) Technical Officer’s Reports

11) Audited/Provisional Financial Statements

12) Status enquiries from other banks regarding the account, promoters or guarantors

13)Account operations scrutiny (Poor turnover, over-dues, frequent returns of cheques/bills, issuing chequesfavouring someone unconnected to main business, withdrawals of large cash, etc.)

14) Statutory Audit Reports

15) Internal Inspection Reports/Special Audit Reports

16) Comments of the Regulatory Authorities

17) Annual review of the account

18) Visits by officials from Controlling Offices to the branches

19) Monthly/quarterly Monitoring Reports and

20) Minutes of Consortium Meetings

The focus of the monitoring process is always to ensure the safety of funds lent and see that the account is conducted as per the terms and conditions of the sanction. It is necessary to understand that recovery of overdue amounts or critical amounts in Standard Assets causing concern is essentially a short-term strategy. An in-depth analysis of the problems facing the borrowing unit has to be made and necessary remedial measures need to be initiated for ensuring long-term viability of the unit.Monitoring function in a bank should cover all the three stages, viz., pre- disbursement, during disbursement and post-disbursement phases of an advance account.

Monitoring –Pre Disbursement Stage

The pre-disbursement stage covers obtaining satisfactory credit reports from existing lenders, post-sanction but pre-disbursement inspection report, execution of the stipulated security documents, including creation of collateral security/mortgage as per terms of the sanction, obtaining letters of guarantee from the guarantors, if any. The other formalities such as vetting of documents by legal experts and ensuring disbursement by the other participating banks and financial institutions are also required as the responsibility of the monitoring department.

Monitoring – Disbursement Stage

During the disbursement, monitoring work should ensure the end-use of the funds by disbursing the amount in the right manner. Credit delivery in loan accounts is distinct from overdraft and cash credit accounts. All disbursements should be related to actual/acceptable levels of performance of the business unit and in line with the basic objective of safety of the banks’ exposure in the credit assets.The disbursement should be commensurate with the progress of the project/business activity, as well as shall take into account the extent of margin brought in by the promoters up to the given point of time.

Monitoring –Post Disbursement Stage

Post-disbursement monitoring forms a substantial part of the monitoring function in a bank. Actual performance of the borrowers should be monitored by inviting select operational data at a particular frequency. The particulars furnished by the borrower need to be compared with the projected performance given to the bank before granting the loans.Periodical inspections and stock audit by the appropriate officials should be ensured. Timely obtention and analysis of the audited financials and review of the account, at least once in a year, is the most integral part of post disbursement monitoring. Timely identification of accounts showing symptoms of strain, and putting them under Watch Category for constant monitoring is absolutely imperative.

Early Warning Signal

Credit Monitoring is an ongoing exercise on each every borrowal account of the bank. No advance can turn bad overnight. The account emits sufficient signals and it is for the banks to constantly observe and capture such signals so that timely remedial action can be initiated to prevent further irregularity and ultimately slippage. An exhaustive list of Early Warning Signals are stated below along with the probable causes and remedy/action that can be initiated against such signals :

Signals noticeable within the bank

| Signals | Probable Causes | Remedies / Action |

| Non-compliance with terms of sanction | Branch failed to explain at the time of giving sanction latter. Casual in nature. Stipulations which are not consented to by borrowers. | Check whether signed copy of the sanction letter is kept on record or not Follow up extensively / visit . Threat to stop operation. |

| Unplanned borrowings for margin contribution | Shortage of fund. Lack of financial discipline. Lack of planning. | Party to adhere to the financial discipline. Educate and advise them to rectify the same immediately. |

| Delay in payment of installment & interest – becoming overdue | Branch has not reminded. Borrower casualapproach. Inadequate cashflow. Activity has come down/stopped. Willful default | Follow up, remind them the due date of installment. Send representatives to collect the dues. Discuss with party for reasons & remedies. Explain the consequences. |

| Return of cheques for insufficient balance | Party may not be depositing the entire sales proceeds. Lack of financial discipline. Shortage of working capital. | Find out the reasons. Check for diversion of funds .Genuine cases, enhance the working capital limit . |

| Chequesissued favoring other banks, chit funds, mutual funds | Loanavailedoutside. Investment in mutual funds. Diversion of funds. | Check end use of funds. View the operations in the account .Ensure money is not going out of system. |

| Reduction in credit summation – | Operating with other bank. Non-realization of Book Debts. Diversion of fund.

Decline in sales. |

Borrower to stop operation with other bank (if any).Recovery mechanism to be strengthened. Insist on bringing back the diverted amount. Find out the reasons and remedy the situation |

| Longer outstanding in Bills purchased | Lack of follow up. Bill of sister concern. Payment problem of the buyers. | Follow up with the paying bank and party .Stopping supply to such buyers |

| Late or non-realization of Bills receivables (Sundry debtors) | Lack of follow up. Bills of sister concern. Lack of financial discipline. Wrong selection of buyers. Lack of market. Probability of embezzlement by salesman. | If needed talk directly to the buyers. Strengthening of recovery mechanism. Find out the root cause.Go for proper selection of buyers .Possibility of offering discounts/incentives |

| Constant utilization of working capital limit upto the brim – even during off seasons | Lack of financial discipline. High debtors.Huge stock of inventory(not required). Sales coming down. Diversion of funds . | Party to bring down the balance. Routing the transactions through account. Party to engage someone for realization of the bills / payment |

| Unexplained delay in submission of periodical statements | Casual approach. Lack of financial discipline. Un-organized office set-up. Problem with working of the unit. | Evaluate the reason for delay .Educate about financial discipline and importance of periodical statementsBranch to visit the unit frequently. Educate about penal provisions & reputation. |

| Frequent request for excess / adhoc or extension of time for repayment | Diversion of fund .Taking high Risk. Lack of financial discipline. Blockage of funds in receivables. Inventory build up. | Evaluate the exact reason .Monitor the a/c operation very closely. Extend the facility on genuine reasons. Enhancement in limit/giving more time. |

| Devolvement of Letter of Credit (LC)& Invocation of Bank Guarantee(BG) | Improper cash flow. Delay in completion of the assigned job. Not keeping up commitments. Incapability in execution. | Forecasting of cash flow not properly drawn. Party to take care for future dealings. Gather information from the beneficiary |

| Avoiding to meet bank officials or lack of transparency in dealings | Business is not running properly. Diversion of fund. May be shifting to other bank. | Branch to visit the unit / party. Evaluate the exact reason. Build confidence – help the party to sort out |

| Failure and unwillingness to mention unpaid stock or age of book debts – Submission of Stock statement in casual manner | Books of accounts not maintained properly. Party not educated properly. Stocks may not be there. | Educate the party the reporting system. Sudden checking of the stock. Engage external agency to evaluate stock .Find out there are any other issues. Insist for CA Certificate. |

| Request of favours of temporary nature like temporary OD, Cheque purchase, Additional LC etc. | May be of genuine reason. Want to avail cash discounts. Diversion of fund. Lack of financial discipline | Request may be considered only in case of genuine reason and within the delegated power. Restructuring, re-phasing may be considered after ascertaining details. |

Signals noticeable by visiting the unit, talking to borrowers/ employees/ market enquiries

| Signals | Probable Causes | Remedies / Action |

| Delay in project implementation | Wrong assessment. Lack of involvement. Delay in supply of machineries. Lack of control. | Find out the reason .Help them to come out of the problem (if possible). |

| Installation of sub-standard machineries or machineries not as per approved quotation | May be a deliberate actIgnorance.

|

Take strong action. Ask the party to replace immediately |

| Frequent breakdown of Plant &Machinery | Poor maintenance. Lack of expertise/skill. Substandard Machine. | Find out the reasons and take remedial steps. Party to explore possibilities for installing new machine .Party to work out the losses |

| Production below projected level of capacity utilization | Absence of expert operators. Lack of raw materials. improper factory setup. Power/labour problems. Lack of demand. | Evaluate the reason. Party to work out the income generation. Party to take all possible action to utilise maximum production capacity. |

| Non-availability of vital spares / raw materials | Locational disadvantage. Machinery is obsolete. Government policies/restrictions | May be temporary in natureReplacement of machinery .Finding out alternate sources. |

| Production of unplanned items | Venturing into new products

Lack of awareness. Less demand for existing product |

Party be cautioned against such activity. Ascertain the reasons for producing such items. |

| Disposal of vital plant machinery without reporting to bank | May be the machinery is not in use. May be deliberate | Ascertain the reason for such activity

Obtain letter from the party. Warning |

| Gradual decrease of sales | Diversion of fund. Non realization of Book Debts. Lack of concentration on Marketing .Production bottleneck. Mismanagement

Poor quality. Increased competition. |

Discussion with party for reasons

Alternate plans. Support required from Bank. Exploring new markets Exit option.

|

| Higher rate of rejection during the process as well as after sales | Poor quality control. Installed poor quality machinery. Use of poor quality of raw materials. Absence of skilled person. | Party to examine the exact reason

Party to call expert immediately to sort out the problem. |

| Delay in payment of statutory dues | Casual in nature. Lack of sufficient cash-flow | Explain that such delay will result closure of business. Ask them to clear all the dues. |

| Diversion of working capital for capital expenses | May be for urgent settlement. Inadequate internal accrual .Lack of planning. May be a deliberate act. | Party to infuse capital immediately

Obtain commitment from the party Ensure production/trading activity is not affected. |

| Abnormal increase in creditors | Suppliers trying to dump the product. Lack of production planning. Inadequate cash flow. Diversion of funds.

Overtrading |

Immediately discuss the reasons

Find out whether corresponding stock/book debt is there. If it is due to under-finance, enhancement be considered |

| Sudden increase in Inventory without justification | Poor performing marketing team. Poor quality Inventory

Production problems. Market issues. |

Ascertain the reason and take action

Dispose off the same by offering discount/cash discount |

| Rapid transfer/attrition of key personnel | Poor HR. Unethical way of doing business | Party to take utmost care during selection of key personnel |

| Unjustified rapid expansion without proper financial tie-up | To have better market share

Improper planning.

|

Discuss with the borrower. Explore the possible reason and take action |

| Dependence on single or very few buyers/ No alternate market for product | Poor marketing network. No much takers for products. May not have explored new markets. | Party be educated the shortcomings for having single buyers. Party to explore other markets |

| Threat of action against the borrower by statutory bodies | Fail to pay the statutory dues. | Explain the outcome of such action.

Party to clear all such dues immediately. |

| Loss of crucial customers | Poor marketing. Poor CRM.

Poor product quality. Availability of better substitutes. |

Ascertain the reason and sort out the problems. Also search for other good customers |

| General decline in particular industry combined with many failures | Government policy. Change in preferences. | Party be asked to take immediate action towards realization. Explore possibilities to venture into other products. |

| Adverse market report on the borrower / concern | Fail to adhere to the market discipline. Poor quality of products. Unethical ways of doing business. Not meeting the commitments. | Discuss with the party and find out the remedy. Engage skilled people. |

| Conclusion

It is the challenging task for the bank to keep the borrowal accounts in standard category and, for this purpose, continuous monitoring of the accounts is necessary .Most of the Banks have installed multiple monitoring mechanism and inspection at different levels viz monitoring by branch managers, officers at controlling offices , audit by external agencies ,RBI, CA firms ,internal audit by head office etc .Inspite of multi –level monitoring systems prevalent in the banks, fresh NPAs are added every year ,enhancing the risk of the loan portfolio. Weakness in credit appraisal and credit monitoring have been identified as major reasons for the accounts turning into non performing assets. It needs hardly to be emphasized that unless monitoring is done effectively , it is impossible to control slippage of standard asset to NPAs .RBI has compiled from their inspections and time to time study and reported a number of lapses and deficiencies in the credit monitoring system of banks. |

Author : M.Ramamoorthy, BE( Mechanical), CAIIB , MBA ( Banking &Finance ) , F.I.V Faculty