The Rise of API Banking: How Open Banking Is Fuelling Embedded Finance

The financial services industry is undergoing a major transformation, driven by rapid technological innovation, rising customer expectations, and progressive regulations. At the heart of this change are API banking and Open Banking.

APIs serves as a tool for providing unique banking services and products. By exposing core banking functions through APIs, Indian banks are transitioning from siloed, branch-led models to agile, platform-centric ecosystems. Regulatory initiatives such as the Account Aggregator (AA) under the IndiaStack framework have further accelerated this shift.

Open Banking in India is not just a global trend but a strategic national initiative to democratize financial access, promote inclusion, and foster a competitive, innovation-driven environment.

An organic evolution of this shift is Embedded Finance, where financial services are seamlessly integrated into non-banking platforms—such as Buy Now Pay Later offers on ecommerce sites, ride insurance by ticketing aggregators etc. This convergence is redefining how and where financial services are consumed.

Understanding API Banking and Open Banking

API Banking

API (Application Programming Interface) banking refers to the use of APIs that enable secure, real-time communication between banks and third-party providers (TPPs). APIs act as digital connectors between systems, allowing developers to build on banking infrastructure to offer a range of services, such as:

- Account aggregation and balances

- Real-time payments and fund transfers

- Credit risk assessment and scoring

- Fraud monitoring and transaction analytics

This has transformed banking from a product-based model into a platform-driven architecture, where financial services can be consumed as microservices within broader digital ecosystems.

Open Banking

Open Banking is a regulatory-led initiative—pioneered by the UK’s CMA and Europe’s PSD2 and now expanding globally—that mandates banks to share customer-permitted financial data with licensed third parties via secure APIs. This access enables fintech’s, aggregators, and non-bank entities to create customer-centric financial solutions, enhancing transparency, competition, and innovation.

In India, the Account Aggregator (AA) framework under the Data Empowerment and Protection Architecture (DEPA) is enabling secure and consent-based financial data sharing, revolutionizing access to credit and financial planning tools.

How Open Banking Fuels Embedded Finance

Embedded finance refers to the integration of financial products into non-financial digital platforms. By leveraging Open Banking APIs, these services become contextual, frictionless, and scalable.

Embedded Payments

- E-commerce platforms like Amazon, flipkart etc offer direct bank account payments via API rails, minimizing card fees and improving conversion. (Amazon Pay).

- Buy Now, Pay Later (BNPL) providers such as ZestMoney, LazyPay, Simpl etc. depend on open banking access for input regarding credit worthiness on real time basis.

Fig 1: Embedded Finance and types

Embedded Lending

- Neobanks like Niyo, Jupiter etc offer microcredit and overdrafts using API-driven data models.

- SME platforms such as moneytap, Aye finance etc provide access to working capital loans by analyzing transactional data via embedded finance partners.

Embedded Insurance

- Travel aggregators (e.g., Booking.com) embed insurance offerings at checkout using insurer APIs.

- Insurtech platforms integrate telematics and financial behaviour data to offer usage-based auto and health insurance.

Embedded Wealth Management

- Robo-advisors like Betterment and Wealthfront use Open Banking data to deliver customized investment advice.

- Super apps (e.g., Phonepe, IND money etc) now offer savings, mutual funds, and micro-investment tools within their core ecosystems.

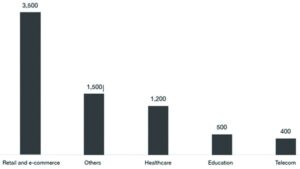

Fig 2: Size of Embedded Finance Market segment wise as on 2030 in USD bn (source: PWC report on Embedded finance: A strategic outlook)

According to a PwC report, the embedded finance market is projected to reach USD 7.1 trillion by 2030, with the largest opportunities emerging in retail and e-commerce, followed by healthcare, insurance, and education. Indicating the huge potential in embedded finance-based services.

Latest Trends and Developments:

Development Trends in Open Banking

- USA: Finalized Open Banking rules (2024) mandating free data sharing and phasing out screen scraping by 2030. FDX is emerging as the standard.

- Canada: Government-led Open Banking rollout; API standards in progress with mandatory compliance under consultation.

- UK: FCA advancing toward Open Finance across pensions, insurance, and wealth.

- EU: PSD2 maturing with tighter fraud controls and AI use; PSD3 and FSR in development to expand Open Finance.

- Australia: Under Consumer Data Right (CDR), Open Banking now includes mortgages, energy, and telecom.

- Singapore & Hong Kong: MAS-led APIX platform and phased Open API rollout shaping fintech collaboration.

- Brazil: Central Bank-led Open Finance covering banking, insurance, and pensions.

- Mexico & Colombia: Advancing toward API-led mandatory frameworks.

- Nigeria: Inception around 2023, working guidelines regarding open banking being discussed.

API Banking: The Rise of BaaS and Embedded Finance

Banking-as-a-Service (BaaS) is enabling non-bank entities to integrate financial services using APIs—without holding a banking license. Global players are capitalizing on this model:

- USA: Apple (with Goldman Sachs) and Uber (with Green Dot, Marqeta) are offering embedded credit and wallets at scale.

- UK & EU: BaaS enablers like ClearBank, Modulr, Solarisbank, and Treezor support digital banks and fintechs.

- India: Fintechs such as M2P, RazorpayX, Open, and Zolve are driving API-first financial innovation under RBI’s regulatory oversight.

- Australia & Singapore: Under frameworks like CDR and APIX, fintechs are launching cross-industry embedded solutions, extending into energy and telecom.

- Brazil: Platforms like Dock and Belvo are powering embedded payments, credit, and wallets across digital channels.

AI-Driven Innovation in API Banking

AI and machine learning are increasingly integrated into API banking systems to:

- Detect fraud in real time through intelligent pattern analysis.

- Provide personalized financial insights via API-powered chatbots (e.g., Erica by Bank of America).

- Enable smarter credit assessments using alternative datasets from embedded finance use cases.

Developmental Trends in India:

Key developments to watch out in the embedded finance and API banking space aided by open banking:

- Account Aggregator (AA) Expansion: By FY26, over 250 million users are expected to be on AA platforms, enabling personalized lending, wealth management, and MSME credit through data-driven models. Integration with OCEN will boost flow-based credit access for underserved segments.

- UPI Growth and Innovation: UPI is projected to exceed 20 billion transactions/month by FY26, driven by features like UPI Lite, credit line linking, voice-enabled payments, and international corridors. Embedded credit and BNPL at POS will see rapid expansion.

- RBI Sandbox Impact: Regulatory sandboxes in payments, lending, and digital governance are expected to incubate 100+ fintech solutions by 2026—enabling innovations in KYC, RegTech, AI compliance, and voice-based banking.

- Public Sector Embedded Finance: Platforms like GeM, eShram, and JanSamarth are embedding credit and insurance services for suppliers and workers, expanding financial access to millions via AA, e-KYC, and UPI rails.

Challenges and Risks

Security and Privacy Concerns

- As API adoption grows, weak or mis-configured API security can expose sensitive customer data, leading to breaches, reputational damage, and penalties under laws such as the Digital Personal Data Protection (DPDP) Act, 2023.

- Ensuring robust consent management under frameworks like the Account Aggregator (AA) system is essential. Users must retain full transparency and control over what data is shared, with whom, and for how long.

Fig 3: Challenges and Risk

Lack of Standardization and Interoperability

- The absence of a uniform framework for data sharing, protection, and access across jurisdictions hampers the interoperability of open banking solutions. For instance, India, the EU, and the USA follow distinct models—Account Aggregator, Berlin Group Protocol, and FDX, respectively.

- Multinational fintechs and NBFCs face higher compliance and integration costs when attempting to scale embedded finance solutions across geographies.

- Within India too, inconsistent implementation across banks and financial institutions leads to friction in on-boarding and interoperability of BaaS offerings.

Business Model Viability

- Many fintechs in India operate on free or low-margin API access models, which are difficult to scale profitably especially with rising cloud costs and tightening regulations.

- Monetization of APIs remains a key challenge, as banks weigh the benefits of open API exposure against data security, regulatory obligations, and the need to preserve traditional revenue streams.

- There is also a growing debate on whether banks should charge third-party fintechs for access to customer data and services potentially impacting financial inclusion goals and overall viability.

The Future of API Banking and Embedded Finance

As regulatory frameworks mature and technology becomes more interoperable, API banking and embedded finance are poised to fundamentally reshape the financial services landscape. The convergence of Open Banking, API banking, and embedded finance will not just expand access but redefine how, where, and by whom financial services are delivered.

From Products to Invisible Experiences

In the near future, financial services will become increasingly contextual and invisible—seamlessly integrated into digital ecosystems that customers already use. Loans, payments, insurance, and investments will be offered on-demand, within apps related to retail, travel, health, logistics, or education—without the user ever needing to interact with a traditional bank interface.

Platformisation of Banking

Banks will evolve into platform providers, offering modular, API-based services that third parties fintechs, startups, and even large consumer brands—can embed into their customer journeys. This shift will encourage banks to unbundle their offerings and focus on core infrastructure, security, compliance, and scalability.

Rise of Hyper-Personalization

With access to rich customer data through APIs and Account Aggregators, banks and partners will be able to offer hyper-personalized financial products tailored to individual behaviours, life stages, and risk profiles—powered by AI and advanced analytics.

Global Interoperability and Standards

The future will also see growing efforts toward global API standards and interoperability, reducing the current fragmentation across geographies and enabling cross-border embedded finance solutions. Regulatory convergence will play a key role in facilitating this evolution.

Implications for Traditional Banks

Traditional banks that fail to embrace this API-first, platform-centric future risk being disintermediated. However, those that invest in robust API infrastructure, collaborate with ecosystem partners, and reimagine their role in a digital-first world will remain central to the future of finance albeit in a very different form than today.

Strategic Implications for Traditional Banks

- Reimagining Role: Shift from being product providers to platform enablers, offering APIs that others can build on.

- Invest in API Infrastructure: Build secure, scalable, and standardized API gateways to support fintech and partner integration.

- Embrace Collaboration: Partner with fintechs, e-commerce, and non-bank platforms to co-create customer experiences.

- Develop Data Capabilities: Leverage consent-based data from Account Aggregators for smarter underwriting, personalization, and risk insights.

- Monetize API Services: Explore sustainable pricing and revenue-sharing models while ensuring compliance with data privacy norms.

- Strengthen Digital Governance: Ensure robust security, consent frameworks, and audit trails to meet regulatory expectations and protect customer trust.

Conclusion

The confluence of API banking, Open Banking, and embedded finance is shaping a future where financial services are ubiquitous, invisible, and intuitive. As APIs become the new financial railroads, banks must evolve from being gatekeepers of services to enablers of innovation.

While the promise is immense, stakeholders must collaboratively address challenges around security, interoperability, and responsible innovation. Harmonized regulations and standardized API frameworks will be crucial for driving sustained growth in the ecosystem.

Ultimately, the financial institutions that embrace openness, build robust API ecosystems, and forge strategic partnerships will lead in this new era. The future of finance is open, interconnected, and embedded transforming how consumers interact with money in the digital age.

Authored by:

Harsh M Sankhala

Research Officer,

SBIIT, Hyderabad